The market has a short memory. When the U.S. dollar began to strengthen in mid-September, this was attributed to the escalation of the trade conflict, a reassessment of market views on the fate of the federal funds rate, a split within the Fed, and the political crisis in France. Investors seem to have forgotten that one of the primary reasons for the USD index's 10% decline in the first half of the year was the White House's desire for a weaker dollar. Donald Trump's visit and his team's trip to Asia served as a reminder of this.

Scott Bessent, in a meeting with his colleague Satsuki Katayama, emphasized that the Bank of Japan must adhere to a reasonable monetary policy. Against the backdrop of a strong labor market and inflation exceeding the 3% target for more than three years, this signals an interest rate hike in the near future. Washington is not pleased with the rapid rally in USD/JPY and is employing verbal interventions. A decline in the pair would mean a weakening of the U.S. dollar, which is precisely what the White House would like to see.

However, the greenback's weakening is progressing slowly. A firm intention from the Fed to continue its monetary expansion amid the de-escalation of the trade conflict, growing global risk appetite, and declining demand for safe-haven assets should have propelled EUR/USD upwards. Nevertheless, the main currency pair is not in a hurry to restore its upward trend.

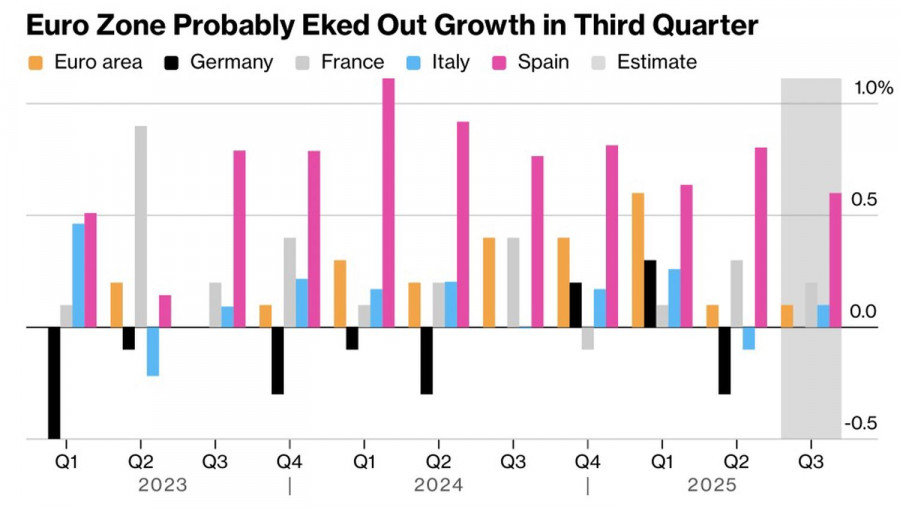

The solid confidence of most Bloomberg experts regarding the end of the Fed's monetary expansion cycle fails to impress the bulls. About 17% of Bloomberg respondents expect a rate hike in 2026. Positive statistics on business activity from the currency bloc and German business confidence are not helping either. Investors are cautiously awaiting the upcoming release of third-quarter GDP data for the currency bloc, which is expected to show 0.1% quarter-on-quarter economic growth.

It would be nice to go to paradise, but sins won't let one in. Despite positive European macro statistics and expectations of hawkish rhetoric from Christine Lagarde following the October Governing Council meeting, the euro faces its Achilles' heel: France's political situation. The parliament may bring another vote of no confidence against Sebastian Lecornu's government if the socialists' proposal to raise taxes on the wealthy is not approved. Someone needs to pay for the budget deficit reduction. Will it be people with low incomes?

Thus, factors such as the de-escalation of the trade conflict, the divergence in monetary policy, and the White House's intention to see a weaker U.S. dollar support EUR/USD. However, France's political situation prevents the euro from mounting a strong attack.

On the daily chart of EUR/USD, a rebound from dynamic resistance in the form of a trend line has occurred. Only a return of prices above 1.167 will increase the likelihood of a recovery of the upward trend and prompt buying. Until then, the risks of the pair consolidating in the 1.159-1.167 range are rising.

RYCHLÉ ODKAZY

ForexMart is authorized and regulated in various jurisdictions.

(Reg No.23071, IBC 2015) with a registered office at First Floor, SVG Teachers Co-operative Credit Union Limited Uptown Building, Corner of James and Middle Street, Kingstown, Saint Vincent and the Grenadines

Restricted Regions: the United States of America, North Korea, Sudan, Syria and some other regions.

Kontaktujte nás

Kontaktujte nás